At Terces Finance, planning is more than spreadsheets. It’s a process. It’s tailored. It starts with listening. Then we map goals, test scenarios, and build a plan that is simple and real. In this post, we show our method and the tools we use. Follow the steps and get clearer money choices.

1. Step 1 — Clarify the goal (listen first)

We begin by listening.

Clients tell us what matters: buying a home, funding education, retiring early, or building wealth.

We ask clear questions. In addition, we record priorities. Then we set measurable goals.

This keeps the plan focused and real.

2. Step 2 — Map the current reality (numbers, not guesswork)

Next, we gather facts. Income. Expenses. Debts. Assets. Insurance. Investments.

We run a cash-flow review. Then we build a clean net-worth snapshot.

This step removes guesswork. It shows what’s possible now.

3. Step 3 — Build scenarios (what-if modeling)

We model multiple scenarios. For example:

- Best case (higher returns, no shocks).

- Base case (likely returns, normal life events).

- Stress case (market drop, job loss, emergency).

Then, we test each scenario. We ask: will the plan survive a market shock? Will the client hit the goal? If not, we adjust. This makes plans resilient.

4. Step 4 — Prioritize simple moves (high-impact, low-friction)

We focus on changes that matter most. Examples:

- Capture employer match.

- Automate savings.

- Rebalance asset mix.

- Reduce high-interest debt.

Small actions add up. Often simple steps close big gaps.

5. Step 5 — Create the plan (actions with dates)

We produce a clear plan. It has:

- Actions (what to do).

- Owners (who does it).

- Deadlines (when to do it).

- Measurements (how we track progress).

Clients leave with a one-page plan. It’s practical. It’s time-bound. It’s easy to act on.

- The Proven Strategy Behind Smarter, More Confident Financial Planning

- FIRE Movement 101: Can You Really Retire Early?

- How Delaying Your Retirement Savings Can Cost You Big

- Think Your Government Pension Is Enough? Here’s Why It’s Risky

- Retirement Planning: How to Win Big in Your 20s—and Catch Up in Your 40s

6. Step 6 — Monthly check-ins & rebalancing

We don’t set and forget, we schedule monthly or quarterly reviews.

Also, we check progress. In addition, we tweak the plan and we rebalance investments if needed.

This keeps momentum and prevents drift.

7. Tools & frameworks we use

We rely on modern tools and proven frameworks:

- Gap calculators (retirement, education).

- Cash-flow dashboards (real-time spending).

- Simple Monte Carlo or scenario simulators for stress testing.

- Low-cost index funds and diversified vehicles for portfolio building.

We avoid complexity. We prioritise cost control and clarity.

8. Real client outcome (mini case study)

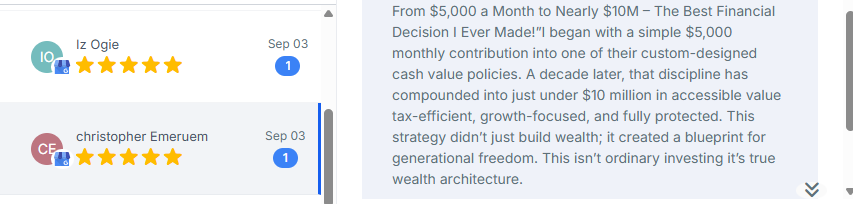

Client A — early 30s (Christopher Emeruem)

- Goal: buy a home in 5 years and build wealth before a decade.

- Action: automated 25% savings, moved to a moderate-growth portfolio, reduced non-essential recurring expenses.

- Result in 24 months: 40% of target saved. Timeline on track. Stress buffer built.

9. Common objections we meet — and how we answer them

- “I don’t earn enough.” → Small, consistent saving works. We start with what’s possible.

- “Market risk scares me.” → We stress-test plans. Then we size risk to the goal.

- “I hate budgeting.” → We use rules, not rigid budgets. Simple rules stick.

10. How you can get started today (quick checklist)

- Write one clear money goal.

- Track your income and spending for 30 days.

- Automate a small transfer to savings (start with 5% if 25% is too high).

- Check if you get an employer match — then claim it.

- Book a short review with a planner if you want help.

FAQs

Q: How long does planning take?

A: Initial planning session is 45–60 minutes. A practical one-page plan is ready within a week.

Q: Do I need a lot of money to start?

A: No. We design plans for any income. Small consistent steps compound over time.

Q: How often will we review my plan?

A: We recommend monthly check-ins at the start, then quarterly or biannual reviews.

Note

Good planning reduces worry. It creates options. At Terces Finance, we turn goals into simple actions. If you want a smarter plan, start with one small step today. Book a review and get a free one-page plan.